For several consecutive years, we have been observing a seasonal spike in Consumer Confidence Index (CCI) coinciding in time with young wine festivals (rtveli) and post-harvest euphoria in rural Georgia. Not this year. In September 2017, CCI lost 2.6 points, going down from -16.4 to -19. Both CCI components, the present situation and expectations indices, declined, by 3.4 and 1.9 points, respectively.

To figure out what happened to consumer confidence in September 2017 we segregated our nationally representative sample into its Tbilisi and rest-of-Georgia portions. The results are striking:

- September was a good, business-as-usual month for Tbilisi residents who continued to gain in consumer confidence, going up from -17.1 in August to -12.6 points in September 2017. This latest monthly improvement of 4.5 points extends a longer term positive trend we have been observing since February 2017, when Tbilisi CCI hit its lowest mark (-25.9 points) in about a year.

- The opposite is true for most Georgian regions. In September, consumer confidence of Georgia’s rural population went down from -15.5 to -24.8 points, more than erasing the gains achieved in August. At least to some extent, this is an outcome of the damage inflicted on Georgia’s agriculture by the so-called marmorated stink bug. This bug has had a devastating effect on hazelnuts, Georgia’s number one agricultural export commodity, reducing export grade produce by at least 20-30% (according to the Georgian minister of agriculture, Levan Davitashvili). Other crops have been damaged as well, triggering protests in Zugdidi, the capital of Georgia’s main hazelnut producing region, Samegrelo.

It is worth noting that the gap in consumer sentiment between Georgia’s rural population and people living in the capital has reached its maximum value (about 12 index points) since we started collecting CCI data. This gap first emerged exactly one year ago, in September 2016, and has been hovering around 6-10 index points ever since.

IT’S THE POLITICAL ECONOMY, STUPID!

Other factors, including government policies, may have contributed to what seems like a permanent relative downward shift in consumer confidence among Georgia’s rural population. For example, as the biggest prize and a must-win jurisdiction in the October 2017 municipal elections, Tbilisi was on the receiving end of massive government investment through much of 2017. Improvements in the city’s public transport infrastructure and street renovation projects, coupled with a highly visible boom in private sector-financed construction projects, may have positively affected people’s perceptions and consumer confidence in the capital.

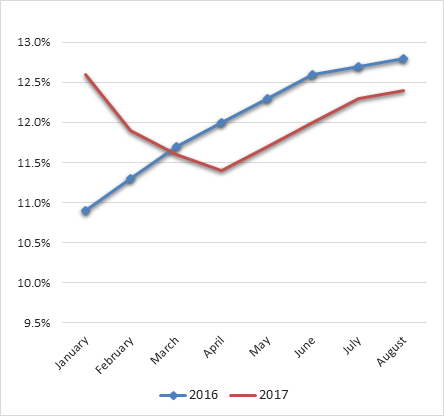

Conversely, Georgia’s rural population was negatively affected by the decline in government-provided social assistance benefits. The number of social assistance beneficiaries has been steadily increasing during 2016, the year of the all-important parliamentary elections, peaking at 12.8% in August 2016. Having won these elections, the government engaged in fiscal consolidation. Thus, in January-April 2017, it cut down on the number of social assistance beneficiaries and relevant budget expenditures. While increasing after April 2017, the number of beneficiaries stayed below its 2016 level. As a result, during the first eight months of 2017, spending on social benefits totaled 5.4% less than in the same period of 2016. While quite reasonable, this policy must have disproportionately hit Georgia’s outlying regions that are characterized by a much higher incidence of poverty.

Share of social assistance beneficiaries in total population, 2016 and 2017

|

|

||||||||||||||||||||||||||||||

| Source: Social Service Agency of Georgia | |||||||||||||||||||||||||||||||

YOUNG VS. OLD

Overall CCI for people younger than 35 has increased by 1.7 index points (from -14.2 to -12.5), in comparison to those older than 35, where the change is in the opposite direction, by -5.1 index points (from -18.1 to -23.2). When looking at sub-indices separately, it becomes clear that older people are more concerned about the present situation. The Present Situation Index for this group moved down by 5.9 points, from -23.8 to -29.7, whereas for the younger group, the same index moved up by 1.1 points, from -16.7 to -15.6. Similarly, the Expectations Index went up (by 2.2 points) for younger people, and down (by 4.3 points) for older people. A straightforward interpretation is that younger people, who can benefit more from reforms and modernization of the society, expected more from the elections than older people.

HIGHER EDUCATION VS. THE REST

Separately computing the Overall CCI for people with and without higher education, one can see that the Index decreased for both groups in September, but to greatly different magnitudes: from -15 to -16.2 (-1.2 points) for people with higher education, and from -20 to -26.6 (-6.6 points) for people without higher education. Apparently, people with higher education are less pessimistic about both the present and future situations.